Why Seattle's Market Makes Downsizing Particularly Compelling

Many Seattle homeowners who purchased in the 1990s or 2000s are sitting on homes worth two, three, or even four times their purchase price. The accumulated equity in those homes represents decades of value-building — and it is entirely illiquid until the home is sold.

In 2026, with the primary residence capital gains exclusion fully intact and mortgage rates creating buyer demand for well-priced smaller homes, the window to extract that equity tax-efficiently and transition into a right-sized property remains favorable. Timing a downsize is a real financial decision — and the current environment rewards it.

What Downsizers Are Really Optimizing For

The language of downsizing often focuses on what is being given up — square footage, guest rooms, the yard. But most people who have navigated the process successfully describe it differently: they talk about what they gained. Lower maintenance costs, a more walkable location, proximity to restaurants and culture, freedom from the burden of a large home.

For empty nesters, in particular, the question of what the extra bedrooms are actually being used for is usually answered honestly only once the children have been gone for a few years. At that point, the cost — in taxes, insurance, maintenance, and time — of maintaining that space becomes difficult to justify.

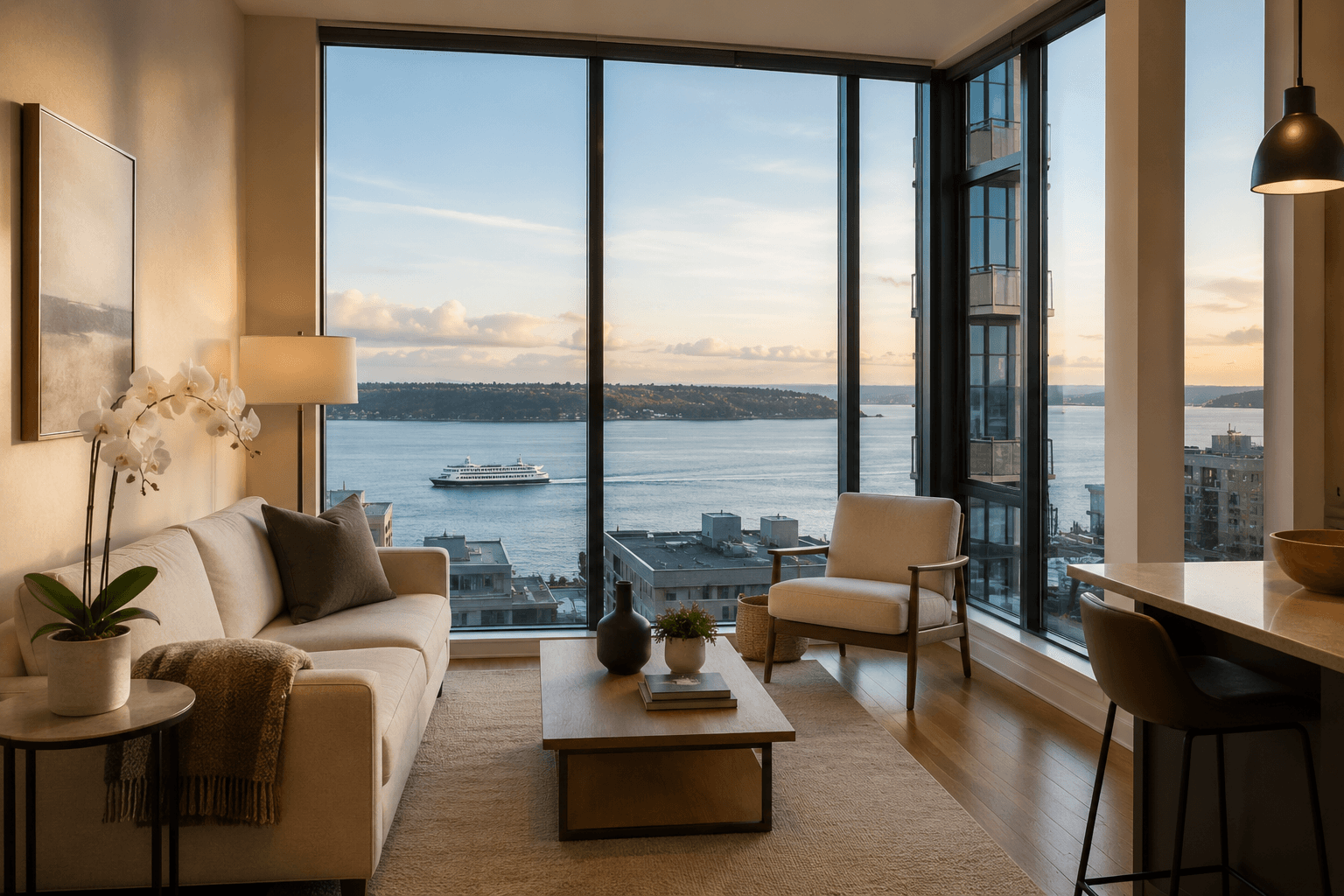

Choosing the Right Neighborhood for Your Next Chapter

Downsizers in Seattle have excellent options across a wide range of neighborhood types. Queen Anne and Capitol Hill offer walkable urban living with high-quality restaurants, cultural venues, and medical facilities within walking distance — ideal for buyers who want to reduce car dependency. Ballard combines neighborhood character with access to waterways and a strong community identity.

Buyers seeking a quieter, low-maintenance lifestyle often find Mercer Island or Bellevue condominiums compelling — concierge services, building security, and amenity-rich environments that support an active lifestyle without the obligations of a yard. The Eastside also offers proximity to excellent medical facilities, which becomes an increasingly relevant factor for buyers in their 60s and 70s.

The Financial Architecture of a Downsize

The ideal downsize involves selling a large home that has appreciated significantly, applying the capital gains exclusion to shelter the gain, and purchasing a smaller home outright or with a minimal mortgage. The difference — the equity freed — can fund retirement, travel, family support, or investment portfolios.

Working with a financial advisor alongside your real estate advisor ensures that the proceeds are deployed in a way that supports long-term financial security. The sequence matters: understanding your tax position before closing, not after, is what allows you to make optimal decisions about the size and structure of the replacement purchase.

The Emotional Side of Letting Go

The homes most Seattle downsizers are leaving were often where their children grew up, where decades of family life unfolded, and where significant personal history is embedded. This emotional weight is real — and it can cause sellers to delay, overprice, or hold on longer than makes financial or practical sense.

Recognizing the emotional dimension and separating it from the financial analysis is one of the most important things an experienced advisor can help with. The process of selling a long-held family home is different from the typical transaction — it benefits from patience, clear communication, and an advisor who understands the weight of what is being decided.

Practical Steps to Start the Process

Begin with an honest assessment of your current home's value — not an online estimate, but a professional opinion from an advisor who knows your specific neighborhood. This establishes the equity you are working with and creates a realistic picture of what a downsize makes possible financially.

Next, define what you actually want in the replacement property: location, maintenance level, proximity to family or medical care, size, and any non-negotiable features. With those parameters clear, the search process becomes focused rather than overwhelming.

Frequently Asked Questions About Downsizing in Seattle

Do I need to sell my home before buying a smaller one? Not necessarily. Depending on your equity position and financial flexibility, a bridge loan or simultaneous close can allow you to purchase the replacement property before your current home goes on the market. This eliminates the stress of the timing gap but involves carrying two mortgages temporarily. Your advisor can walk through the options based on your specific situation.

What size should I downsize to? There is no formula — it depends on how you live. Many downsizers find that 1,400 to 1,800 square feet with smart layout design and high-quality finishes feels more spacious and functional than a 3,200-square-foot home that was partly underutilized. Quality of space matters far more than quantity.

Should I sell first or buy first? In a competitive market, having your current home under contract or sold gives you stronger negotiating position as a buyer. In a softer market, buying first can make sense. Your advisor should help you assess which approach fits the current market dynamics.

The best downsizes are not retreats — they are strategic moves toward a more intentional version of the life you want to live. In Seattle's market, they can also be among the most financially rewarding decisions a homeowner ever makes.